Introduction

Understanding Scope 1, 2, and 3 emissions is essential for businesses aiming to manage their environmental impact. These categories provide a clear framework for identifying where emissions originate, both within operations and across the value chain. By breaking emissions down in this way, organizations can set meaningful reduction targets, track progress, and contribute more effectively to global climate goals.

The GHG Protocol Corporate Standard, developed by the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD), provides a standardized framework for measuring and reporting GHG emissions, covering seven gases listed in the Kyoto Protocol (CO2, CH4, N2O, HFCs, PFCs, SF6, and NF3).

The protocol classifies a company’s GHG emissions into three ‘scopes’ — Scope 1, Scope 2, and Scope 3 for corporate-level emissions inventories. These GHG emissions are released across a company’s entire value chain.

Here’s a simple classification of the three, before we get into their complexities to understand how Scope 3 emissions are different from Scope 1 and Scope 2 emissions.

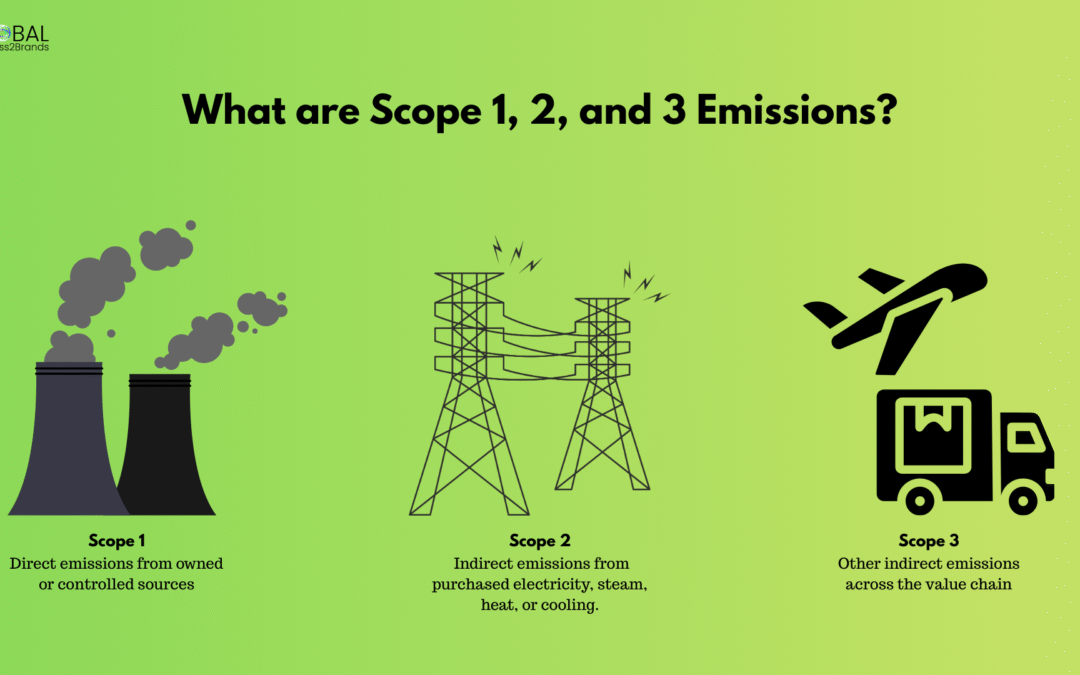

- Scope 1: Direct emissions from owned or controlled sources (e.g., company vehicles, on-site fuel combustion).

- Scope 2: Indirect emissions from purchased electricity, steam, heat, or cooling.

- Scope 3: Other indirect emissions across the value chain (e.g., supply chain, employee commuting, product use), as detailed in the Corporate Value Chain (Scope 3) Standard.

Scope 1 and Scope 2 Emissions Explained:

Scope 1 emissions come from sources the company directly controls (like its vehicles), while Scope 2 emissions are tied to purchased energy used by the company but generated elsewhere.

Scope 3 Emissions Explained: What makes them complex?

Scope 3 emissions are all indirect emissions that are not included in Scope 2 that occur in a company’s value chain, both upstream and downstream, but are not directly owned or controlled by the company. These are often the largest and most complex category of emissions to measure and manage.

Key Categories of Scope 3 Emissions

The GHG Protocol’s Corporate Value Chain (Scope 3) Standard outlines 15 categories, including:

- Upstream: Purchased goods and services, business travel, employee commuting, transportation and distribution (e.g., shipping raw materials).

- Downstream: Use of sold products, end-of-life treatment (e.g., disposal/recycling), transportation and distribution of sold products.

The production cycle phases typically include raw material acquisition, manufacturing/processing, distribution, use, and end-of-life. The table below outlines how Scope 1, 2, and 3 emissions align with these phases, with examples specific to the metal parts manufacturer.

| Production Cycle Phase | Scope 1 Emissions | Scope 2 Emissions | Scope 3 Emissions |

| Raw Material Acquisition | None (company does not directly control raw material extraction). | None (no purchased energy in this phase). | Supplier raw material extraction & processing (e.g., steel production emissions). |

| Manufacturing/Processing | Emissions from on-site fuel use, e.g., natural gas for factory furnaces. | Emissions from purchased electricity for factory machinery. | Emissions from outsourced manufacturing processes or employee commuting to the factory. |

| Distribution | Emissions from company-owned delivery trucks. | None (distribution typically does not involve purchased energy). | Third-party logistics, outsourced shipping. |

| Use | None (company does not control product use). | None (no purchased energy in this phase). | Customer use of products (e.g., electricity consumed by appliances). |

| End-of-Life | None (company does not manage disposal). | None (no purchased energy in this phase). | Recycling, disposal, or treatment of sold products. |

Note: Emission sources shown align with each production phase and emission scope. Actual greenhouse gas values (e.g., CO2) depend on specific fuels, electricity grid factors, and detailed lifecycle data.

Why Scope 3 Matters ?

Scope 3 emissions often account for the majority of a company’s carbon footprint (sometimes 70-90%) but are harder to measure due to reliance on external data from suppliers, customers, and partners. For example, a company’s direct emissions (Scope 1) and electricity use (Scope 2) might be small compared to emissions from its supply chain or product use.

GB2B offers advisory services, helping your organization with comprehensive measurement and reporting of greenhouse gas emissions.

Conclusion

The path to Net Zero is clear but challenging, requiring comprehensive action across all emissions scopes. By leveraging the GHG Protocol’s Scope 1, 2, and 3 framework, organizations can quantify their carbon footprint, address value chain impacts, and lead the charge toward a sustainable future. Collective commitment to these standards will turn our climate ambitions into reality.

Neha

Neha is a seasoned professional who blends academic rigor with hands-on experience in content strategy and corporate communications. With a career spanning startups, NGOs, and multinational banks, she brings a deep understanding of sustainability challenges across industries. A passionate advocate for environmental justice, Neha has actively contributed to impactful campaigns, driving awareness and action on critical environmental issues.

As an academician, she specializes in economics, financial services, banking, insurance, and management principles—providing her with a strong analytical foundation to decode complex ESG trends for businesses. Through her writing, Neha delivers insightful, data-driven perspectives that help B2B audiences navigate the evolving sustainability landscape with clarity and confidence.